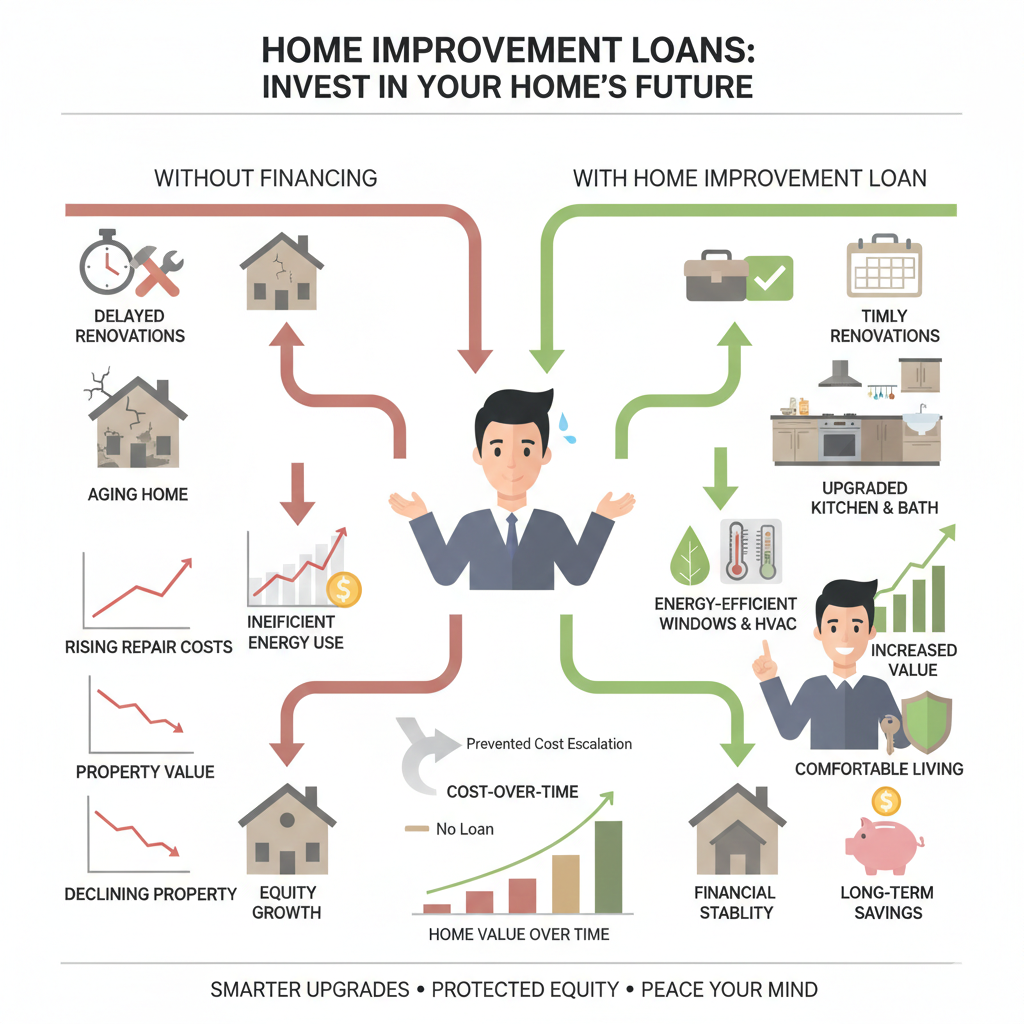

Home improvement financing in 2026 is no longer just about “getting a loan.” Rising interest rate sensitivity, stricter credit underwriting, energy-efficiency incentives, and evolving homeowner priorities have changed which loan types make financial sense and when.

Whether you’re renovating to increase resale value, reduce energy bills, or adapt your home for long-term living, choosing the right home improvement loan can save (or cost) you tens of thousands of dollars over time.

This guide reviews and compares the best home improvement loan options in 2026, explaining how they work, why lenders price them differently, and which option fits specific renovation goals based on current lending trends.

Why Home Improvement Loans Matter More in 2026

As of 2025–2026, three major shifts are influencing renovation financing decisions:

-

Higher borrowing costs mean loan structure matters more than ever

-

Energy-efficient upgrades now deliver measurable ROI through lower utility costs and tax incentives

-

Home equity levels remain historically strong, even with cooling housing markets

Well-planned renovations especially kitchens, bathrooms, insulation, HVAC, and accessibility upgrades continue to deliver some of the highest returns among consumer investments. Financing them strategically preserves liquidity while maximizing long-term value.

How We Evaluated the Best Home Improvement Loans (2026 Criteria)

Each loan type was reviewed using modern borrower priorities:

-

Total cost over time, not just APR

-

Speed vs flexibility trade-offs

-

Risk exposure to your home

-

Suitability for phased vs one-time projects

-

Approval accessibility in 2025–2026 lending conditions

Types of Home Improvement Loans Explained

1. Personal Loans for Home Improvement

Best for: Fast, mid-sized renovations without using home equity

Personal loans remain popular in 2026 because they’re unsecured, fast, and predictable. However, higher benchmark interest rates have widened the gap between secured and unsecured borrowing.

Why Personal Loans Work (and When They Don’t)

They make sense when:

-

You need funds quickly

-

You don’t want to risk your home

-

The project cost is limited

They become expensive when used for long-term or large renovations due to higher interest.

Pros

-

No collateral required

-

Fixed interest rates

-

Funding often within 1–3 business days

Cons

-

Higher APRs than equity-based loans

-

Lower borrowing limits

-

Less cost-effective beyond 5–7 years

2026 Insight: Personal loans are best for projects with short payoff timelines, such as cosmetic upgrades or urgent repairs.

2. Home Equity Loans

Best for: Large, one-time renovations with predictable costs

A home equity loan functions like a second mortgage, offering a lump sum at a fixed rate. In 2026, lenders favor borrowers with strong equity buffers and stable income.

Why Equity Loans Offer Lower Rates

Because your home secures the loan, lenders assume less risk resulting in:

-

Lower interest rates

-

Longer repayment terms

-

Higher borrowing limits

Pros

-

Fixed monthly payments

-

Lower APRs than personal loans

-

Easier budgeting

Cons

-

Home is collateral

-

Slower approval process

-

Closing costs may apply

Best for: Additions, full kitchen remodels, or structural upgrades.

3. HELOC (Home Equity Line of Credit)

Best for: Phased or ongoing renovation projects

HELOCs provide revolving access to home equity. As of 2025–2026, most HELOCs have variable rates tied to benchmark indexes, which introduces both flexibility and risk.

Why HELOCs Are Strategic (and Risky)

They shine when:

-

Costs are uncertain

-

Work happens in stages

-

You want interest-only payments during construction

But rising rates can increase payments unexpectedly.

Pros

-

Borrow only what you need

-

Interest-only options during draw period

-

Ideal for long projects

Cons

-

Variable rates

-

Payment shock after draw period

-

Home-secured risk

4. FHA 203(k) Rehab Loans

Best for: Buying or refinancing fixer-uppers

The FHA 203(k) loan remains one of the most underutilized but powerful renovation tools in 2026 especially for first-time buyers.

Why FHA 203(k) Still Matters

It combines:

-

Purchase or refinance

-

Renovation costs

-

Single mortgage payment

This lowers the barrier to entry for buyers who lack large cash reserves.

Pros

-

Low down payment (3.5%)

-

Lenient credit requirements

-

Covers major repairs

Cons

-

Contractor restrictions

-

Longer approval timeline

-

No luxury upgrades

5. Cash-Out Refinance

Best for: Homeowners with older, higher-interest mortgages

A cash-out refinance only makes sense in 2026 if your new mortgage rate doesn’t significantly exceed your existing rate.

When Cash-Out Refi Works

It’s effective when:

-

You already plan to refinance

-

The renovation is large

-

You want one consolidated payment

Trade-Off

You’re resetting your mortgage clock and reducing equity.

6. Credit Cards (Use With Caution)

Best for: Small, urgent, or short-term expenses

Credit cards remain a bridge solution, not a financing strategy.

They work only when:

-

You can repay during a 0% APR period

-

The cost is small

-

Speed matters more than cost

Comparison Table: Home Improvement Loan Options (2026)

Loan Type |

Secured |

Rate Type |

Typical APR (2026) |

Best For |

|---|---|---|---|---|

Personal Loan |

No |

Fixed |

7%–36% |

Fast, mid-size projects |

Home Equity Loan |

Yes |

Fixed |

5%–8% |

Large, one-time remodels |

HELOC |

Yes |

Variable |

6%–10% |

Phased renovations |

FHA 203(k) |

Yes |

Fixed |

5.5%–8% |

Fixer-uppers |

Cash-Out Refi |

Yes |

Fixed |

5%–7.5% |

Major renovations + refinance |

Credit Card |

No |

Variable |

16%–29% |

Emergency fixes |

How to Choose the Right Home Improvement Loan in 2026

Match Loan Type to Project Size

-

Under $5,000: Savings or 0% APR card

-

$5,000–$25,000: Personal loan or HELOC

-

$25,000+: Home equity loan, FHA 203(k), or refinance

Consider Risk vs Cost

Lower rates often mean higher risk. Ask yourself:

“Am I comfortable using my home as collateral for this project?”

Alternatives Worth Considering in 2026

Energy-Efficiency Incentives

-

Federal tax credits for insulation, HVAC, solar

-

Utility rebates

-

State-level green loan programs

Contractor Financing

Convenient, but often embedded with higher effective rates.

401(k) Loans

Low interest, but high opportunity cost and repayment risk if employment changes.

Frequently Asked Questions (People Also Ask)

Are home improvement loan interest payments tax deductible?

Only if the loan is secured and used for substantial home improvements. Always consult a tax professional.

What credit score do I need in 2026?

-

Personal loans: 620+

-

Equity loans/HELOCs: 660+

-

FHA 203(k): As low as 580

Which loan is cheapest overall?

Home equity loans usually have the lowest total cost, assuming stable rates and long-term repayment.

Can I combine loan types?

Yes some homeowners use a HELOC for construction and refinance later into a fixed loan.

Final Thoughts: Financing Home Improvements in 2026

The best home improvement loan in 2026 isn’t the one with the lowest advertised rate, it’s the one that aligns with your project timeline, risk tolerance, and long-term financial goals.

By understanding how each loan works, why lenders price them differently, and where real costs accumulate, homeowners can renovate smarter not just faster.

![HubSpot CRM Review: Is It Worth It in 2025? [Full Expert Breakdown]](https://radical.fm/wp-content/uploads/2025/08/1-10-360x180.png)

{kind=link}